Gold prices will plunge in coming weeks, according to one of the strongest correlations you’ll ever see in the markets. Except you shouldn’t put any weight on this correlation.

This doesn’t mean gold won’t decline. But a correct assessment of gold’s prospects has to be based on more than a statistical pattern that has no theoretical foundation. That’s the case with one that has many gold bugs worried.

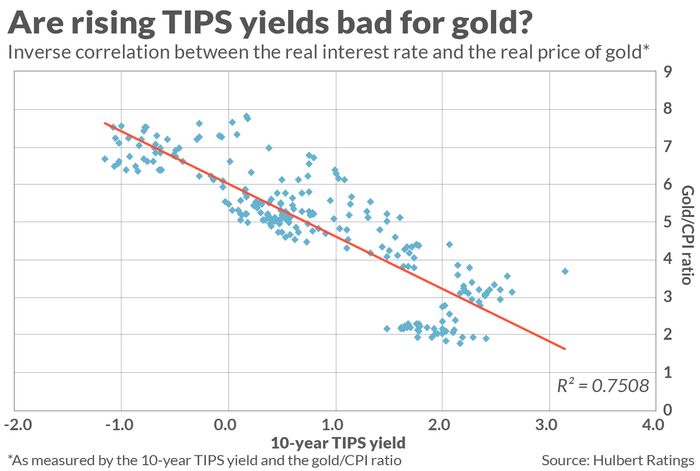

I’m referring to the inverse correlation between the real interest rate (as measured by the yield on 10-year Treasury Inflation-Protected Securities, or TIPS ) and the real price of gold

GC00,

(as measured by the ratio of gold’s nominal price to the Consumer Price Index). As you can see from the chart below, the r-squared of this correlation is a statistically impressive 0.75. Historically, 75% of the changes in one of these data series has predicted or explained the changes in the other.

To put this r-squared in context: Most of the patterns that capture Wall Street’s attention have r-squareds close to zero, even if they are statistically significant — which is rare.

If this correlation is meaningful, gold could be in big trouble. Claude Erb, a former commodities fund manager at TCW Group, said in a recent email that if you were to believe this inverse correlation will persist into the future, its message is that gold is overvalued. If the TIPS yield were to rise even more, gold would need to fall even further to become fairly valued.

The key question, then, is whether to believe this correlation will persist. Erb does not, pointing out that correlation is not causation. He has compelling reasons to question it, which he advanced several years ago in a study he co-wrote with Campbell Harvey, a Duke University finance professor. I refer you to that study for a fuller discussion of these reasons, and I’ll briefly summarize them here.

1. Unknown direction of causality: One of the reasons is that, even if correlation in this case were causation, we still wouldn’t know the direction of the causality. “While it is possible to argue that historical data suggest that low real yields ‘cause’ high real gold prices…, it is equally possible to argue that causality runs in the other direction and that high real gold prices actually ‘cause’ low real yields.” If that were the case, then the investment implication of the correlation would be that real interest rates are likely to be lower in coming weeks and months. The correlation would provide no insight into where gold is itself headed.

2. Correlation far different in the U.K. than in the U.S: Another reason to question the strong inverse correlation between gold’s real price and real interest rates in the U.S. is that the corresponding correlation in the U.K. is much weaker. The r-squared in the U.K. is just 0.09, according to Erb and Harvey, hardly enough to write home about. I know of no theoretical reason why it should be so much different in the U.S. and the U.K., and the existence of this discrepancy raises serious doubts about the correlation’s meaning and reliability.

3. No plausible theory for why the correlation should exist: Perhaps the most compelling reason to question what the correlation might be telling us is that there is no plausible theoretical justification for why it should exist. This is a crucial point, since it’s possible to discover myriad correlations with even more impressive r-squareds but which are nevertheless meaningless. An example Erb and Harvey give in their study is the correlation between the historical price of gold and time, which has an even higher r-squared than the correlation between gold and interest rates. The implication of this correlation is that gold’s price always goes up and will eventually reach infinity, which is not only unhelpful for market timing purposes but also “hard to grasp,” as Erb and Harvey write.

In a recent email, Erb provided another example of a spurious correlation: Between the real price of gold and the amount of atmospheric CO2 measured at the Mauna Loa Observatory in Hawaii. Erb calculates that this correlation is just as strong as between real interest rates and the real price of gold. Needless to say, there is no theoretical explanation for why gold’s price should be related to greenhouse gasses.

The bottom line? Unless you can tell a plausible story for why there should be an inverse correlation between real interest rates and the real price of gold, and in turn a plausible story for the direction of causality between the two, the correlation is little more than, as Erb said quoting Ralph Waldo Emerson, “the foolish consistency” that is the “hobgoblin of little minds.”

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at [email protected]

More: Gold has disappointed. Here’s what could change that.

Plus: A strong dollar is stirring trouble in markets: What investors need to know