Only about one-fifth of the S&P 500 have so far reported second-quarter results, but at least five major talking points have emerged — some quite surprising — since earnings season started more than a week ago.

A key concern heading into earnings season wasn’t what happened during the previous three-month period, but how much companies would lower forward guidance, given growing fears the Federal Reserve’s aggressive interest rate increases to fight historically high inflation would tip the U.S. economy into a recession.

But with 106 of the 503 S&P 500 companies having reported results through Friday morning, according to FactSet, that expected negative has so far been a positive.

For the second quarter, while more companies than usual are beating profit and revenue expectations, they’re beating them by narrower-than-usual margins.

So far, so good

Through Friday morning, 75.5% of the companies reporting have been beating consensus analyst projections for earnings per share, by an average of about 4.7%, according to I/B/E/S data provided by Refinitiv. That compares with 66% of companies beating EPS estimates in a typical quarter since 1994, and an average beat margin of 9.5% for the prior four quarters.

And for revenue, 68.9% of the companies have topped forecasts by an average of about 1.3%, compared with 62% of companies beating in a typical quarter since 2002 and an average beat rate of 3.4% for the prior four quarters.

More beats by less than the usual amount has led to year-over-year growth in the blended EPS estimate, which includes results from companies that have already reported results and estimates of companies yet to report, to slip to 5.0% from an estimate of 5.7% growth as of March 31, according to FactSet data.

The blended estimate for revenue growth has increased to 10.7% from 9.7% at the end of March, FactSet said. That’s because companies are not selling more but are selling at higher prices.

Meanwhile, despite worries that recession fears would lead to a raft of full-year guidance cuts, that just hasn’t been the case. In fact the ratio of negative EPS preannouncements to positive preannouncements has so far been 1.7, according to I/B/E/S data, well below the long-term average of 2.6, and only slightly above the average over the prior four quarters of 1.5.

As a result, the FactSet consensus growth estimate for EPS has increased to 9.7% from 9.3% as of March 31, while the growth estimate for revenue has jumped to 10.4% from 8.9%.

Jeff Buchbinder, equity strategist for LPL Financial, said earnings are “well on track” to grow by more than 5% from last year, given “solid” beat rates and “healthy” revenue growth, bolstered by higher pricing.

“We believe the revenue environment and corporate productivity are in too good of shape for earnings to contract anytime soon,” Buchbinder said. “Bottom line, the pessimism may be overdone.”

Yes, dollar strength is a headwind

That said, there was a worry heading into earnings season that is being fulfilled: The sharp rise in the U.S. dollar will reduce the value of profits and revenue generated from overseas operations.

Also read: A strong dollar is stirring trouble for markets: What investors need to know.

Here’s why a rising dollar can hurt results of multinational companies: The U.S. dollar-Japanese yen exchange rate increased to 135.75 on June 30 from 122.50 on April 1, meaning 10,000 yen in earnings was worth just $73.66 on June 30, down from $81.63 on April 1.

So with the U.S. dollar index

DXY,

which tracks the dollar against a basket of currencies of major trading partners, surging 6.5% during the second-quarter, the biggest quarterly gain since the fourth quarter of 2016, currency translation had a large negative effect on earnings.

For example, International Business Machines Corp.

IBM

said earlier this week that second-quarter revenue growth was 9%, but would have been 16% if not for the negative effects of dollar strength. And Dow Inc.

DOW

said on Thursday that currency decreased sales by 3%, while Johnson & Johnson

JNJ

said unfavorable currency translation reduced its sales growth by 5%.

“This will be a consistent theme that receives significant attention throughout the earnings season,” said Lindsey Bell, chief markets and money strategist for Ally, especially for the technology sector, in which nearly 60% of the sectors revenue is generated overseas.

Snap confirms a grim outlook for big internet companies

Fears that ad-supported internet stocks were facing a perfect storm of issues that would show up in second-quarter earnings were realized this week, when Snapchat parent Snap Inc.

SNAP

posted what one analyst called “terrible” numbers, as others rushed to downgrade the stock.

Snap missed revenue consensus estimates and executives declined to provide a financial forecast while speaking of a second quarter that was “more challenging than we expected.” Snap had already warned weeks back that it was bracing for disappointing performance.

The company is dealing with issues unique to the evolving social-media landscape as well as a broader macroeconomic storm. Not only does it have to deal with TikTok’s rise and lingering privacy-related impacts from Apple Inc.

AAPL,

it’s also facing an ad-market slowdown that spooked analysts.

Read now: As Snap melts down, its founders make sure to protect the people who matter: themselves

“Results suggest a significant deterioration in advertiser demand, which will likely weigh on the sector,” Piper Sandler analyst Thomas Champion wrote in a note to clients late Thursday.

“When fundamentals change this dramatically, it’s hard for us not to change our investment opinion, however belated the call,” said Evercore’s Mark Mahaney, who cut his rating on Snap’s stock to in line from outperform.

“We will await a stabilization in revenue growth before considering getting more constructive,” he added.

MoffettNathanson downgraded the stock to market perform. Among other gripes, the analysts there said that “after spending many years denying that competition from TikTok is an issue, it may turn out that Snap’s usage and advertising growth is actually far more challenged than they knew.”

For more, see: Snap’s dire ad warnings prompt string of downgrades: ‘This stock faces a grim outlook’

The report bodes ill for other internet giants that rely on digital ads, including Meta Platforms Inc.

META,

Alphabet Inc.

GOOGL

and Apple, all of which report next week

Don’t miss: It’s the end of ‘fantasyland’ for Big Tech and its workers

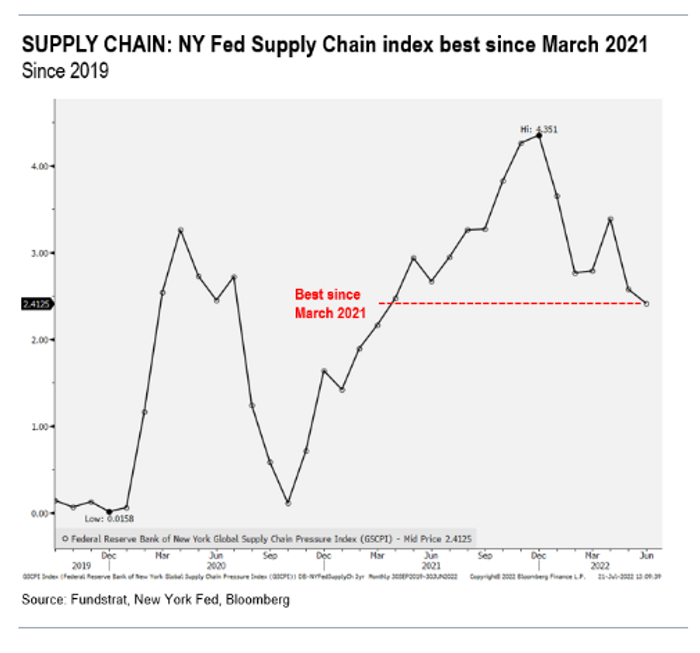

Supply chain and labor shortages are still key themes

The supply chain and labor shortages have featured prominently in earnings for the past several quarters and this one is no different so far.

But there are finally some signs of improvement in supply chains, as measured by certain indexes.

The NY Fed’s supply chain index is currently at its best level since March of 2021 — it hit its worst level in December of 2021, as Tom Lee, head of research at Fundstrat Global Advisors, noted in commentary.

Lee cited upbeat comments from Volvo AB

SE:VOLV,

which said semi chip access was improving and production at best levels all year, and railroad operator CSX

CSX

which said there are “clear signs” from car makers that chip challenges are easing.

And on Thursday, chemicals giant Dow Inc. said it had “higher supply availability” for its industrial solutions and for its coatings & performance monomers business.

The news on the labor market is less cheery, however. The challenge of finding train conductor trainees, for example, led Norfolk Southern Corp.

NSC

to put out an unusual release, highlighting an increase in hourly pay to a minimum of $25 and biweekly on-the-job training incentive of $300.

Atlanta, Ga.-based Norfolk said conductor trainees in priority locations can earn up to $5,000 in starting bonuses and expect first-year pay of an average $67,000, along with benefits including a pension, a 401 (k) savings option and healthcare coverage

Those locations include some economically depressed ones: Bellevue, Ohio, Fort Wayne, Indiana, Binghamton, New York, Harrisburg, Pennsylvania, Cincinnati, Ohio, Louisville, Kentucky, Conway, Pennsylvania, Peru, Indiana, Decatur, Illinois, Princeton, Indiana, Elkhart, Indiana and Roanoke, Virginia.

The challenge of finding railroad workers showed up in CSX’s earnings too. Chief Executive Jim Foote told analysts on the company’s earnings call that it was having trouble hiring and retaining workers.

“We are not alone in facing this problem,” said Foote, according to a FactSet transcript. “The labor market is tight. Prospective recruits have many job options.”

Read now: ‘People will freak out’: The cloud boom is coming back to Earth, and that could be scary for tech stocks

Twitter may be right. Elon is hurting its business

When Twitter Inc.’s lawyers asked a Delaware judge Tuesday for a speedy trial that would settle its merger spat with Elon Musk, they argued that the saga’s overhang was causing constant harm to the company.

That topic came up again when Twitter

TWTR

reported downbeat financial results Friday, including a surprise dip in revenue and a sizable $270 million loss. Among factors the company blamed for its revenue miss was “uncertainty related to the pending acquisition” by Musk. The company also pointed to about $33 million in second-quarter costs related to the deal.

Twitter didn’t elaborate further in its earnings release, nor did it hold a conference call, so investors are left to wonder how exactly the Musk dispute impacted the company’s revenue. The company’s legal filings and arguments hold some clues about what the company may mean. Lawyers argued in a written complaint that Musk’s “derogation” of the deal close and his “repeated disparagement of Twitter” and its employees “create uncertainty and delay that harm Twitter and its stockholders” while opening the company up to adverse business effects.

At Tuesday’s hearing, Twitter’s legal team discussed employee unease due to uncertainty over the deal. It’s possible that Twitter is having trouble retaining employees during a tumultuous period, or that turmoil around the deal is impacting the ability to roll out projects effectively and on time.

“It does seem like there’s turmoil amongst employees and even among the board,” said Carl Tobias, a law professor at the University of Richmond. “The future of the company just doesn’t seem very clear.”

A Twitter representative said that the company was not providing additional details on revenue performance beyond what was in the release.

Twitter also mentioned a tougher advertising backdrop as another reason for its revenue performance. Given building unease about the state of the ad market in the weeks leading up to Twitter’s report and the dire signals sent by Snap earlier in the week, it’s likely that ad-market challenges are more to blame for Twitter’s top-line woes than the ill-defined Musk effects.

For more: Twitter has more to worry about than Elon Musk

But there could perhaps be a link as well: In a rocky climate for ad spending that’s seen brands tighten their belts, marketers may be opting for safer platforms that aren’t the source of controversy over bot activity.

{kind=link}