The Federal Reserve isn’t even four months into its latest interest-rate -hiking cycle, and yet investors are already pricing in rate cuts as soon as next year, the latest sign that the market is bracing — or perhaps rather hoping — for a swift return to the easy-money monetary policy that helped drive the roaring stock market of the years following the 2008 financial crisis.

Deutsche Bank economist Jim Reid pointed out in his latest “Chart of the Day” note sent to the German investment bank’s clients that the Fed funds futures market, a derivatives market that allows investors to place bets on the direction of the Fed’s interest-rate policy, is already anticipating a pivot back toward easy monetary policy at some point next year. After the Fed Funds rate reaches its current market-expected peak of 3.39% in February 2023, investors expect the central bank will start cutting interest rates again, which would be tantamount to declaring “victory” over inflation.

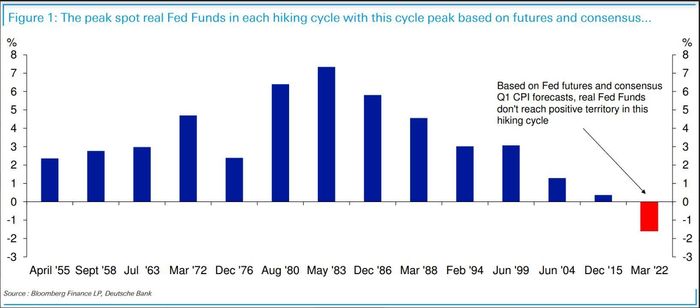

But will such a brief stretch of tighter policy be enough to help defeat inflation? As Reid points out, if the expectations turned out to be accurate, this would raise an interesting issue for the Fed: it would mark the first time in 70 years that the level of the Fed’s benchmark interest rate target failed to surpass the rate of inflation during the entirety of a rate hiking cycle.

Right now, markets expect that in “real” terms — that is, when adjusted for inflation — the Fed Funds rate won’t reach positive territory at any point during this tightening cycle.

Fed Chairman Jerome Powell has repeatedly acknowledged that many of the factors contributing to high inflation are outside of the Fed’s control. The Fed can’t magically order commodity prices lower, and it can’t solve the war in Ukraine, or any lingering supply chain issues caused by Beijing’s response to the latest COVID outbreak.

In fact, the whole point of raising interest rates is to hopefully stifle the economy and weaken the American labor market, leading to higher unemployment and a drop in demand.

It’s also notable that investors expect the tightening cycle to be over in roughly a year. The Fed raised interest rates in March for the first time since late 2019.

How unusual would such a short tightening cycle be? Looking at the last few rate-hike cycles, there have been a couple that were shorter than 2 years: one cycle lasted from February 1994 to July 1995 . Another lasted from June 1999 to January 2001. Others have been longer. The cycle of rate hikes that preceded the Great Financial Crisis in 2008 began in June 2004 and ended in September 2007. By comparison, the cycle that began in December 2015 and concluded in August 2019 lasted almost four years, although the Fed opted for a much more cautious pace during this cycle.

Source: Deutsche Bank

But it certainly seems notable that markets aren’t anticipating positive real interest rates while the Fed tries to take on the most aggressive inflation since the early 1980s.

Which leads Deutsche’s Reid to pose a critical question for markets: are investors being too sanguine? After all, if expectations start to shift to favor a more aggressive pace of tightening from the Fed, then that could drive more pain in both bonds and stocks.

Worries about slowing U.S. economic growth were weighing on stocks on Tuesday, with the Dow Jones Industrial Average

DJIA,

down more than 600 points. The S&P 500

SPX,

was down 1.9% to 3,754. Meanwhile, the yield on the 10-year Treasury

TMUBMUSD10Y,

had fallen more than 9 basis points to 2.793%.