There’s been such a rush to buy “I-bonds,” inflation-protected bonds from the U.S. government, that the TreasuryDirect website crashed.

I-bonds have been one of the hottest investments of the year. People who never talk about investments have been telling me about the I-bonds they’ve been buying. Market strategists have been asking me if I’ve bought my I-bond allocation “yet.”

Investors who bought before Friday’s deadline locked in an interest rate of 9.6% (briefly), which will tumble to an estimated 6.5% if you missed it.

Well, you can count me out. I haven’t been rushing to buy I-bonds, and I am baffled by the euphoria they seem to engender. I think they are overall a pretty mediocre deal, and there is something much better.

Why are they a mediocre deal? Well, you’re limited to $10,000 worth a year (you can squeeze that to $15,000 if you overpay your federal taxes and get a refund—no thanks). The interest is fully taxable. You have to hold them for five years to get the full interest. That “9.6%” interest is an annualized version of the 6 monthly return, and is poised to plunge. Oh, and most important of all (maybe), is that the so-called “real” return is bupkis: Zero.

A “real” return is what economists call your rate of interest in constant dollars: In other words, your rate in purchasing power terms, after adjusting for inflation. (If an investment has, say, an 8% rate of interest, but inflation is 8%, it has an 8% “nominal” return but a 0% “real” return.)

The reason I’m not interested in I-bonds has nothing to do with inflation. It is clearly here, it has clearly metastasized from energy prices, and it may prove to be much more persistent than Wall Street currently seems to assume.

But if, like me, you are worried about the risks of persistent inflation there are alternative investments that I find much, much more compelling than I-bonds. They offer a better return. They offer the same federal guarantee. And yet they are largely ignored by the stampeding hordes frantically clicking “refresh” on the TreasuryDirect website.

I am talking about TIPS: Treasury inflation-protected securities.

These are bonds, or IOUs, issued by Uncle Sam and backed by the same full faith and credit of the United States Government that you get from T Bills, 10 Year Treasury notes and so on. But they come with a twist. Instead of guaranteeing to pay you a fixed rate of interest, like traditional U.S. Treasury bonds, they guarantee to pay you a fixed rate of interest every year on top of inflation.

And right now, while I-bonds are paying a “real” rate of interest of 0%, or inflation plus 0%, long-term TIPS are beating that by nearly 2 full percentage points a year.

You can buy unlimited amounts of TIPS. You can own them in tax sheltered retirement accounts. Oh, and they are simple to buy. You can buy individual TIPS bonds directly through any broker. Or you can own them through a mutual fund or exchange-traded fund, such as the Vanguard Inflation Protected Securities Fund

VAIPX,

iShares TIPS Bonds ETF

TIP,

iShares 0-5 Years TIPS Bond ETF

STIP,

or Pimco 15+ Year U.S. TIPS ETF

LTPZ,

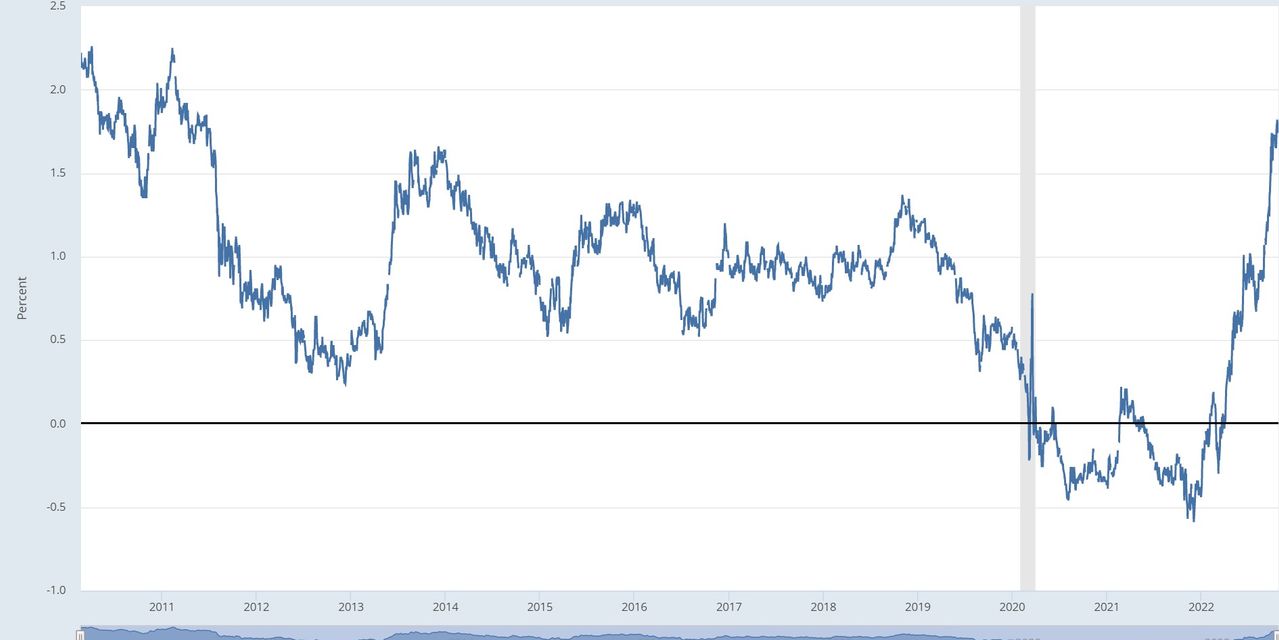

Check out the chart above. It shows the average “real” return on 30 Year TIPS bonds, and how it’s changed over time. The higher the line, the better the return. Right now we’re getting the best offer in over a decade. Thirty-year TIPS bonds will pay you inflation plus about 1.8% a year. 10-year TIPS bonds will pay you inflation plus about 1.6%.

If I buy the 10-year and hold it until it matures in 2032 I am guaranteed to end up 16% richer in real, purchasing-power terms, no matter what happens to inflation over the next decade. That is completely risk-free.

And if I buy the 30 year bond and hold it until it matures in 2052 I am guaranteed to end up by then 70% richer in real purchasing power terms.

And I won’t care in the slightest what happens to inflation. Won’t effect me. It will just pass straight through into a higher interest rate on my bond.

Let the record show that the long-term average return on stocks has traditionally been much higher, somewhere between 5% and 7% a year on top of inflation (depending on who is counting it and how). These TIPS returns should be understood in terms of a “risk-free” asset, not in terms of the (probably) higher long-term returns you can earn from risky ones.

Right now the 10 year TIPS bond pays inflation plus 1.6%, while the regular, (non-inflation-adjusted) 10 Year Treasury bonds pays a fixed 4% a year. So the regular Treasurys will only be a better bet if inflation averages 2.4% a year or less over the next decade.

Good luck with that.

TIPS have rallied in the last few days. That means the price for some has risen a bit, and the interest rate has fallen. (Bonds work like a seesaw: When the price goes up the yield or interest rate goes down, and vice versa.) But the rates of interest are still compelling.

TIPS are something of an orphan asset class, which may be why they seem to be overlooked. Institutions and investors who want “Treasury bonds” typically just buy the regular ones, which pay a fixed rate of interest.

TIPS were first created by the U.S. government in the late 1990s. They were following the British government, which created its own in the 1980s. But both were created only after the runaway inflation of the 1960s and 1970s. So they have never (yet) been used for the reason they were created, namely to protect you against sustained, year-over year inflation. I sometimes think of them as fire insurance in a city that hasn’t yet had a major fire.

This may be why TIPS prices have tanked this year, even during an inflation panic. Investors have dumped all bonds, and the longer-term the bonds the worse they have fallen. It also didn’t help that TIPS came into the year heavily overvalued by most rational measures: The TIPS bonds that will pay you positive real returns if you buy them today were paying 0%, or even negative real returns, if you bought them late last year.

The PIMCO 15+ Year U.S. TIPS Index ETF

LTPZ,

has fallen nearly 40% so far this year, nearly as much as the Vanguard Extended Duration Treasury ETF

EDV,

This makes little or no logical sense unless you simply view TIPS as another kind of bond. Long-term nominal bonds lose value in an inflation spiral because all those future interest payments are worth much less in real, purchasing power terms. The same is, by definition, not true for TIPS bonds.

Legendary British money manager Jonathan Ruffer has been banging the drum about TIPS—and inflation—all year. So far the prices have fallen, a long way. Maybe he is wrong about them. Or maybe he was just way too early.

Former U.S. “bond king” Bill Gross recently came out for short-term TIPS.

TIPS have one major potential downside compared to I-bonds: If you buy TIPS through an ETF, or if you buy individual bonds and then sell them before they mature, you can in theory lose money. That’s because the price moves around—as we’ve seen this year. Theoretically if you buy them well above face value you could also lose money if we suffer years and years of deflation (which hardly seems likely).

On the other hand, I’ve been buying individual TIPS bonds at, near or even below face value, and I would be happy holding them till they mature. So I’m not worried. I am guaranteed to get back the face value, plus all the accumulated inflation over the period I hold the bond, plus the interest.

My biggest risk is “opportunity cost.” If I buy a long bond paying inflation plus 1.8%, I could miss out: The bond could keep falling, and someone who waits could get an even better deal. And if I own a TIPS bond earning inflation plus 1.8% a year, and the stock market earns you inflation plus 6% a year, I will also miss out.

(Over 30 years, incidentally, an asset earning 6% a year in “real” terms will leave you 470% richer, not 70% richer.)

And while they can go down in price, they can also go up. Indeed, two weeks ago I was having dinner with a money manager in London who had predicted this year’s crash, whose fund is up for 2022, and who said their biggest bet was in long-term bonds, mainly TIPS and British equivalents. They figure these will pay off if there is an economic crash (people will want bonds), a recovery (interest rates will probably come back down, and people will also want bonds), or sustained inflation (people will want inflation protection).

Make of it what you will. If long-term TIPS keep going down you can have a laugh at my expense. But so long as I hold on to my investments, I am guaranteed to make money in the end—no matter what happens.