A summer rebound is stirring hopes the bear market in U.S. stocks has seen its lows, but a meeting of Federal Reserve policy makers this coming week might test the nerves of would-be bulls.

“I expect we will continue to see market volatility until investors have seen more convincing evidence that this period of Fed hawkishness is behind us, and I do not expect that to be the message” when central bankers conclude a two-day meeting on July 27, said Lauren Goodwin, economist and portfolio strategist at New York Life Investments, in a phone interview.

Disappointing results from social-media platform Snap Inc.

SNAP,

trimmed a weekly rise in stocks on Friday, but the benchmark indexes still saw healthy gains. The S&P 500

SPX,

rose 2.6% in the past week to end near 3,962 after pushing above the 4,000 threshold early Friday for the first time since June 9. The Dow Jones Industrial Average

DJIA,

logged a weekly gain of 2%, while the Nasdaq Composite

COMP,

advanced 3.3%.

The bounce this week lifted the indexes off 2022 lows after the S&P 500 sank to a finish of 3,666.67 on June 16.

See: Is the stock-market bottom in? What the pros say after S&P 500 tests 4,000

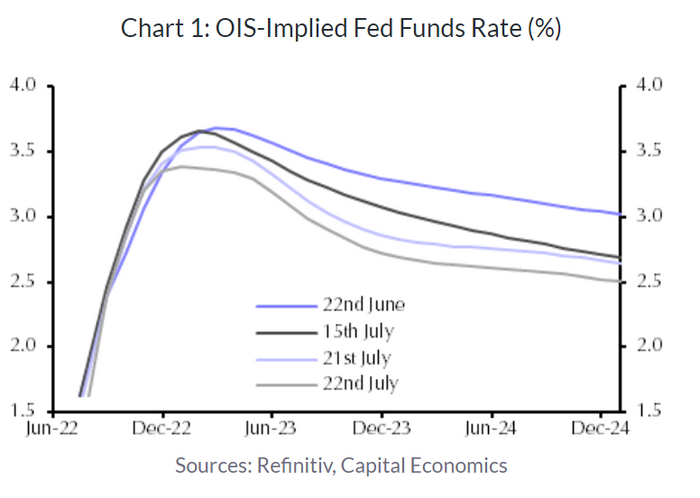

The rebound has been fueled in part by a dynamic that’s seen investors treat bad news on the economic front as good news for stocks, said James Reilly, an economist at Capital Economics, in a Friday note.

That may sound strange, but it likely reflects, in part, a view among investors that weaker economic data will lead the Fed to raise interest rates less than previously thought, Reilly wrote. There’s evidence for that in market-based expectations for rate increases, which have been pared back lately (see chart below), a development that has provided support for equity valuations, he said.

Capital Economics

Market expectations are for the Fed to deliver a 75 basis point interest rate increase on Wednesday, matching the increase seen in June, which was the largest since 2002.

Read: The Fed could get lucky or things might go wrong. A guide to where the economy might go from here

Meanwhile, the past week delivered plenty of evidence of slowing economic activity.

The U.S. services purchasing managers index fell to a 26-month low of 47 in July from 51.6 in the prior month, based on a “flash” survey from S&P Global Market Intelligence. A reading of less than 50 signals a contraction in activity.

On Thursday, weekly jobless claims rose to the highest level since November but remained historically low, the Philadelphia Fed manufacturing index unexpectedly fell deeper into negative territory, and the Conference Board said its leading economic index shows that a U.S. recession around the end of the year and early next is now likely.

U.S. economic data due next week include a first estimate of second-quarter gross domestic product, that’s expected to show a second straight contraction. While such an outcome is often described as a technical recession, a still strong labor market and other factors are seen making it unlikely the National Bureau of Economic Research, the official arbiter of the business cycle, will declare one.

Related: A ‘fake’ recession? The U.S. economy is in decent shape for now despite weak GDP

Reilly said he doubts slowing activity will slow the Fed’s roll.

“Our central forecast is that U.S. economic growth will remain weak, but not so weak as to deter the Fed from hiking aggressively over the rest of this year. Such an outcome would probably mean rising discount rates and disappointing growth in corporate profits, which would be a fairly toxic combination for equity prices,” he wrote.

Many Fed watchers, including some ex-policy makers, see a Fed intent on convincing market participants of its desire to snuff out inflation.

Former Richmond Fed President Jeffrey Lacker on Friday said policy makers would need to keep raising interest rates even if there is a recession. “To let your foot up off the brake before inflation has come down” is just a “recipe for another recession down the road,” Lacker said, in an interview on Bloomberg Television.

Even if the economy slowed fast enough to cause Fed policy makers to back off, it probably wouldn’t be great news for equities, Reilly argued. That’s because corporate earnings would weaken further than the firm already expects, he said. It’s also unlikely that the support equities have seen as expectations for the fed-funds rate have moderated would continue in a severe slowdown, with history showing that valuations have tended to fall during such periods as appetite for risk deteriorated.

Goodwin, however, said there’s more to the stock market’s recent resilience.

“The market, on average, was anticipating a tougher earnings season than what we’re seeing so far,” while guidance has also been more upbeat, she said, acknowledging that it’s still early days.

Through Friday morning, 75.5% of the S&P 500 companies that had reported have beaten consensus analyst projections for earnings per share. The average was by about 4.7%, according to I/B/E/S data provided by Refinitiv. That compares with 66% of companies beating EPS estimates in a typical quarter since 1994, and an average beat margin of 9.5% for the prior four quarters.

On revenue, 68.9% of the companies have topped forecasts by an average of about 1.3%, compared with 62% of companies beating in a typical quarter since 2002 and an average beat rate of 3.4% for the prior four quarters.

Earnings Watch: Here are 5 things we’ve learned so far from earnings season

Markets have been dominated by worries over red-hot inflation and the threat of recession, so a “somewhat more sanguine” read from companies so far was a dose of good news, Goodwin said.

Indeed, investors have seemed to cycle between fears over inflation and recession, market watchers said. Red-hot inflation was the dominant worry as stocks tumbled and Treasury yields soared in the first half of 2022. More recently, market action indicates investors have focused more on the prospect of recession as the Fed aggressively tightens policy.

So what should investors do as the focus shifts from inflation toward recession ?

Goodwin said inflation will remain a primary consideration when it comes to portfolio positioning because recession-resilient assets, such as cash, Treasurys and high-grade corporate bonds that worked in the last cycle can create a significant drag on wealth creation.

To deal with expected volatility, New York Life is moving up in quality within asset classes. For example, it’s strongly overweight high-yield debt in its portfolios on expectations the corporate environment will remain pretty robust, she said, but is moving up in quality within high yield.

Keeping rising consumer prices in mind, it also means looking at equity and fixed-income securities that have cash flows linked to inflation, she said.