If stock market FOMO is starting to bug you, but you’re hesitant to buy stocks, here’s a fix: Go small.

Small companies are still super-cheap.

These aren’t companies whose CEOs grab headlines when they speak. You may not even have heard of most of them. But when you buy their stocks, you are investing in the economic heart and soul of the U.S. Small companies employ most people in the country. You probably work for one.

Here are three reasons why they look attractive.

1. The smaller, the better

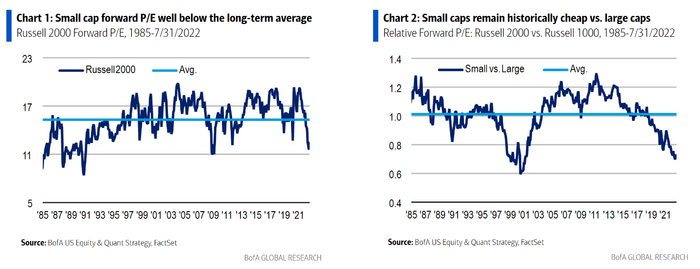

The Russell 2000 Index

RUT,

which tracks smaller companies, recently traded at a forward price-to-earnings (P/E) of 12.4. That is 19% below its historical average (since 1985). In contrast, the Russell 1000 Index

RUI,

of larger-cap names trades at a forward P/E of 17.5 times. That is 13% above its average.

Put another way, the relative forward P/E of the Russell 2000 is 0.71 time the Russell 1000 forward P/E, below its average of 1.01 times. (These data come from Bank of America researchers Jill Carey Hall and Nicolas Woods, in a note published this week.)

This value differential implies vast outperformance for small companies, say Hall and Woods. It suggests 12% annualized returns for Russell 2000 small-cap names over the next 10 years vs. 7% for the larger-cap Russell 1000 names. Small companies are generally a good place to have part of your long-term investments. Since 1926, smaller companies have posted a compound annual growth rate (CAGR) of 12% vs 10% for the S&P 500 Index

SPX,

notes William Blair economist Richard de Chazal.

But Bank of America offers this important warning: Think long term. This is not a prediction about what will happen to small stocks tomorrow, or next month.

“Valuation tends to be a poor short-term timing indicator, but it matters much more for long-term,” says the bank.

However, in my view, you may not have to wait too long for outperformance. Why? So-called smidcap — small- and mid-cap — names tend to outperform in a bull market as investors desire riskier assets, and I believe a new bull market has emerged since the mid-June lows.

Smidcaps have market values of $1 billion to $10 billion. They include the likes of Crocs

CROX,

and Texas Roadhouse

TXRH,

Large-caps are $10 billion and up. The Russell 1000 large-cap index includes giants including Apple

AAPL,

Microsoft

MSFT,

and Alphabet

GOOGL,

2. Investors will warm up to ‘smidcaps’

Judging by sentiment indicators, investors are clearly still not in full risk-on mode. But they’ll get there. Just give them time. Why?

Inflation is coming down, which reduces the risk that the Federal Reserve will create a recession. Besides, the economy actually looks sound. The Atlanta Fed GDPNow estimate for third-quarter GDP was moved up to 2.5% from 1.4% Aug. 10.

“We won’t be surprised if real GDP for Q1 and Q2 eventually are revised from down slightly to up slightly,” says Ed Yardeni of Yardeni Research. “This is shaping up to be a year of slow growth, but not of recession.”

As investors figure this out, they will take on more risk and buy smidcaps. That’ll drive them up. That means the time to buy them is now, before they do.

3. Inflation-beaters

Inflation is not going back to 2% quickly, so this advantage will remain important. Why does inflation help small-cap companies relative to large-caps? Small companies are nimbler on pricing, says de Chazal at William Blair. In contrast, larger-cap companies have entrenched pricing models and layers of management. That makes them the “supertankers” of price flexibility. It takes them more time to adjust. Also, small companies typically have fewer long-term investment projects. The long-term investment projects at big companies are trickier to manage profitably when prices are volatile.

The best sectors and stocks

In small-cap land, it’s best to favor energy and financials, says Bank of America. Their view is based on analysis of which sectors have the best upward earnings estimate revisions, relative valuations, price momentum and stock rating changes inside B of A. The bank says go easy on health care, communications services and utilities.

I’ll add cyclicals as a group to favor, since it seems like growth is picking up after the slowdown phase, judging by the recent uptick in jobs growth, the ongoing inflation decline which will boost consumer confidence, and the Atlanta Fed GDPNow increase in third-quarter growth estimates.

To find small-cap names that are still reasonably valued, I think it makes sense to go with the ones where insiders are telling us valuations are good — because they are buying their own stocks.

Energy stocks: I’ll suggest Empire Petroleum

EP,

and Comstock Resources

CRK,

I put Empire Petroleum in my stock letter (the link is in the bio, below) on July 15 at around $9.40 a share and the stock is already up 48%. But I still like it because the company collected energy assets in the oil patch during 2018 through early 2021 before energy prices took off. Presumably it got good deals. It has a strong balance sheet to support more acquisitions. Insiders bought about $815,000 in stock at prices up to $12.35 in June. At $14 a share, the stock is not too far above that now.

The natural gas company Comstock Resources also recently saw some insider buying in size when an officer purchased $428,000 worth of stock at $14.86 on Aug. 8. Comstock has been buying natural gas assets lately. The insider purchase looks like a signal that they got some good deals that will pay off for shareholders.

Financial stocks: In banking, it’s hard not to like Texas Capital Bancshares

TCBI,

because a director recently bought $3.7 million worth of its stock in July, and $5.7 million since then at prices up to $58.84. Bank stocks have been held back by the inverted yield curve. This suggests loans (priced at the long end of the curve) net less than the cost of funds (priced at the short end). But if there is no recession, as I believe, or at least not a deep one, the yield curve will revert and banks will be OK. Texas Capital Bancshares is a mini-turnaround because it is moving into new areas like trading and new loan types. Judging by the 33% second-quarter revenue growth and 11% loan growth, the strategy seems to be paying off.

Cyclical stocks: For help finding recent compelling insider purchases, I turned to The Washington Service, which specializes in analyzing insider activity. They single out Hudson Pacific Properties

HPP,

Univar Solutions

UNVR,

and Woodward

WWD,

Cyclicals like these tend to outperform when the economy expands.

Hudson Pacific is a real estate investment trust (REIT) investing in office buildings and production studio properties in California, the Pacific northwest, western Canada and London. It serves tech and media companies, which are economically sensitive. Revenue grew 16% in the second quarter. Washington Services says the director who purchased at $13.94 has an excellent track record.

Univar Solutions supplies specialty chemicals and ingredients used in industry, pharmaceuticals, food and other consumer products. This makes it an economically sensitive, cyclical company. The director who recently purchased stock at $25.68 has a solid record at his company and several others, says Washington Service. Univar recently posted 30% second-quarter sales growth and 6.3% growth in net income.

Woodward provides parts and control systems used at industrial and aerospace companies. The company posted solid 10% second-quarter sales growth, but earnings slipped due to inflation and supply chain problems — issues that will improve. A director who sold a lot of stock last year at much higher prices, reversed course in early August and bought $1 million worth at $95.86 a share. He’s got a good track record, says Washington Service, and such insider reversals can be a bullish signal.

Of course, you can mitigate individual stock risk by also owning the iShares Russell 2000 ETF

IWM,

Michael Brush is a columnist for MarketWatch. At the time of publication, he owned AAPL, MSFT, AMZN, GOOGL, and EP. Brush has suggested AAPL, MSFT, AMZN, GOOGL, EP and CRK in his stock newsletter, Brush Up on Stocks. Follow him on Twitter @mbrushstocks.