Housing’s in freefall. Big Tech is slowing down. Even at Coca-Cola

KO,

which surprised to the upside for the third quarter, CEO James Quincey flagged “there are some changes in consumer behavior going on.”

So of course, the U.S. stock market is starting to rev higher, with the S&P 500

SPX

up five of the last seven sessions, though it’s looking like Wednesday could be rough after Alphabet and Microsoft results. The market is forward looking, to a time when the Fed sees a need to cut interest rates, rather than hike them to choke off the economy.

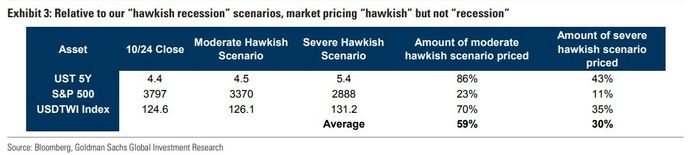

Strategists at Goldman Sachs say the move feels premature. “Because we have not decisively met either of the two conditions—convincing inflation relief or a shift towards outright recession—that we think are necessary for a sustained shift, we do not think the pressure for tighter financial conditions is at an end,” they say.

The strategists — Kamakshya Trivedi and Dominic Wilson — say there has been “inching,” in their words, toward both conditions. “So after a sharp tightening, the threshold for some near-term relief is lower,” they said.

But the issue is that inflation news could still disappoint. “If the Fed slowed the pace of hikes and subsequent inflation news disappointed, energy prices moved materially higher or financial conditions eased sharply, they might find themselves pushing back against the market relatively quickly or risking uncomfortable pressure on back-end yields. So unless the inflation news turns convincingly better, we could still find ourselves back in the [financial conditions] loop relatively soon,” they said.

The other big risk is that a severe recession develops. No asset, they say, is priced for a big downturn, though the rates markets and the U.S. dollar are pricing in a greater possibility than the stock market or corporate credit.

The strategists conclude by saying “the broader case for U.S. equities does not look very strong and the normal conditions for an equity trough are not clearly visible yet. Equities have not fully reflected the latest rise in real yields and any significant easing in financial conditions through higher equities will likely be offset by policy in the end.”

The markets

U.S. stock futures

ES00

NQ00

fell sharply, though the Dow industrials

YM00

contract wasn’t as bad. The U.S. dollar

DXY

was lower, thanks to a big rally in the British pound

GBPUSD

as the euro

EURUSD

topped $1. The yield on the 10-year Treasury

BX:TMUBMUSD10Y

fell to 4.07%.

The buzz

Google parent Alphabet

GOOGL

fell 6% in premarket trade as the company reported lighter-than-forecast revenue, hurt by weakness in online ad spending. Microsoft

MSFT

shares also fell 6% on slowing revenue from its cloud business Azure, as the company guided for cloud revenue growth of around 30% in the current quarter.

Amazon

AMZN,

which reports Thursday, was pressured by the Microsoft results, due to its Amazon Web Services cloud business.

Facebook parent Meta Platforms

META

reports after the close.

Intel’s

INTC

self-driving unit, Mobileye

MBLY,

priced its IPO at $21, which was above the $18 to $20 per share range. Texas Instruments

TXN

lowered guidance for the fourth quarter.

The advanced trade in goods report is due at 8:30 a.m. Eastern, along with estimates of retail and wholesale inventories. Shortly after the open, new-home sales are due for release.

The U.K. pushed back its fiscal plans to the middle of November on day two of Rishi Sunak’s premiership.

Best of the web

Those on Capitol Hill said it was “painful” to watch Democratic nominee John Fetterman, who had a stroke, debate Mehmet Oz in the pivotal Pennsylvania Senate race.

Just 26 of 193 countries that agreed last year to step up their climate actions have followed through with more ambitious plans.

Russian oligarchs obscure their wealth through a British island.

Top tickers

Here were the most active stock-market tickers as of 6 a.m. Eastern.

Random reads

A survey finds a third of young adults have been going to horror movies, while Gen X and boomers have said, “Nope.”

The world’s dirtiest man refused to use soap and water for more than half a century. He finally did and died a few months later.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Listen to the Best New Ideas in Money podcast with MarketWatch reporter Charles Passy and economist Stephanie Kelton.