A pullback in the U.S. dollar earlier this week was credited with helping to lift a rallying stock market, but one strategist isn’t convinced U.S. currency has peaked.

The dollar extended its losses against other major currencies on Thursday after data showed July wholesale prices cooled a day after encouraging headline consumer price index data. The ICE U.S. Dollar Index

DXY,

a measure of the currency against a basket of six major rivals, rose 0.6% on Friday but was on track for a 0.9% weekly fall.

Stocks, meanwhile, continued a rally off their mid-June lows, with the Nasdaq Composite

COMP,

exiting bear-market territory this week, while the Dow Jones Industrial Average

DJIA,

and S&P 500

SPX,

were also on track for strong weekly gains.

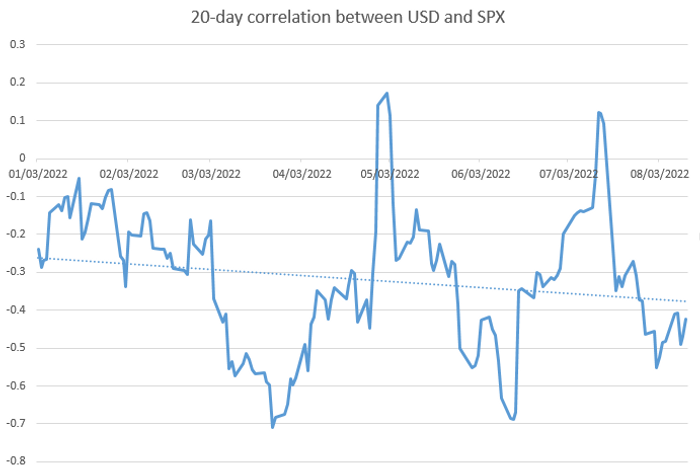

“The USD and SPX both move together but especially at the extremes. When the USD squeezes higher is when the SPX is squeezing lower and visa-versa,” said Brad Bechtel, global head of FX at Jefferies, in a note on Thursday. “Same on the reverse side as well as we have seen over the past 24 hours or so.” (See chart)

SOURCE: DOW JONES MARKET DATA

The euro

EURUSD,

breached $1.0350, “but we need a close above the $1.0380 level to target a run towards the 1.0530 100-day moving average,” he wrote. The DXY is heavily weighted toward the euro.

The euro

EURUSD,

traded at $1.026 on Friday afternoon, keeping the U.S. dollar index

DXY,

within touching distance of the two-decade highs it reached last month.

The dollar has been weakening since the middle of July, when the euro briefly fell below parity to the dollar as traders boosted bets that surging inflation in June would force the Fed to hike its benchmark interest rate by as much as 100 basis points to a range of 2.5% to 2.75% at its July meeting. These moves pushed the dollar index up 1.2% to 109.29 on July 14, its highest since 2002. The Fed delivered a 75 basis point rise at its July meeting.

On the flip side, according to Bechtel, it’s not the end of the euro’s weakness versus the dollar as Europe is planning to start winter with historically low amounts of natural gas and other fuels. The European Union sanctions on Moscow in response to the invasion of Ukraine in April have resulted in Russian exports of gas slowing through the Nord Stream 1 gas pipeline, the single largest link for Russian gas supplies to Europe. Fears are growing of the potential for a full-blown energy crisis, including gas rationing and soaring energy bills, during the European winter.

“I do not think the USD has peaked, but a lot depends upon how bad the winter gets for Europe,” Bechtel told MarketWatch on Thursday.

Meanwhile, hopes that inflation has peaked helped encourage investors to pile back into equities based on the view that slowing inflation could allow the Fed to hike interest rates less aggressively. U.S. stocks on Friday were on track to cement their longest weekly winning streak since November with the S&P 500 rising 1%, while the Dow gained 0.8% and the Nasdaq jumped 1.4%. However, some analysts didn’t believe the back-to-back inflation reports were strong enough to change the Fed’s approach.

“The Fed is still going to be hiking and remain aggressive on inflation,” Bechtel said. “So I think the market is a little ahead of itself in thinking the Fed is going to let financial conditions remain easy.”

See: Can the stock market bottom without Wall Street’s fear gauge hitting ‘panic’ levels?

This notion was also shot down by San Francisco Federal Reserve Bank President Mary Daly, who favored the latest CPI and PPI prints, but said a 50 basis point rate hike is her base case at the September 20-21 policy meeting, according to a Bloomberg interview on Thursday. She was also open to a 75 basis point hike, citing some improvements in inflation are not enough to convince the board that they have had a “victory”.

Treasury yields were lower Friday with the yield on the 2-year Treasury note

TMUBMUSD02Y,

rising to 3.244% from 3.227% on Thursday. The 10-year Treasury yield

TMUBMUSD10Y,

fell to 2.859% compared with 2.886% Thursday.