Last week, the U.S. dollar etched a new entry in the financial history books when it briefly traded above parity with the euro

EURUSD,

for the first time in a generation.

While the greenback has pulled back from its highs this week, banks in Europe and the U.S. — including UBS Group, ING, Credit Suisse, Rabobank and JPMorgan Chase & Co. — generally expect the dollar to continue to strengthen heading into the end of the year. Indeed, investment banks generally don’t expect the dollar rally to start to reverse until next year.

After peaking north of 108, a gain of roughly 17% for the year, the ICE U.S. Dollar Index

DXY,

has pulled back over the past week though. It’s now roughly 12% higher at 107, against a basket of rival currencies.

Dollar drivers

Credit Suisse analysts explained that the dollar’s strength this year has been driven by three primary factors.

- Interest-rate differentials: Higher interest rates and higher bond yields in the U.S. have made the dollar more attractive for international investors, since they can pick up a higher yield on their dollar-based deposits and bondholdings.

- Growth differentials: COVID-inspired shutdowns in China, and the war in Ukraine, have prompted investors to bet that the U.S. economy will fare better than rivals in Europe and Asia over the next year.

- Flight to quality: Fears about a global recession have prompted investors to seek “safe haven” assets like the dollar.

The dollar’s strength also appears to correspond with weakness for U.S. stocks. Credit Suisse estimates that for every 8% to 10% move in the dollar, corporate profits in the U.S. retreat by a full percentage point.

With this in mind, it probably shouldn’t come as a surprise that the dollar’s recent pullback has coincided with a rally this week in U.S. stocks, since the dollar has exhibited a strong negative correlation to equities and other “risky” assets this year.

The dollar has been one of the few safe-haven assets with a strong performance in 2022. Over the past seven months, the dollar has outperformed other “safe” assets like gold and Treasurys.

It hasn’t only been the yen and the euro that have been weakening. Vanishingly few currencies have outperformed the dollar this year, especially in the emerging-market space. To date, the greenback has gained more than 7% against the South African rand

USDZAR,

more than 10% against the South Korean won

USDKRW,

and more than 6% against the Chinese yuan

USDCNY,

(if one uses the exchange rate for the “offshore” yuan, which isn’t as closely managed by the People’s Bank of China).

Analysts at ING blamed the dollar’s recent pullback from its strongest level since the early 2000s on “a growing narrative of other central banks closing the gap with the Federal Reserve” following an unexpected 100 basis point rate hike from the Bank of Canada, and reports that the European Central Bank plans to raise its benchmark rate by 50 basis points on Thursday, instead of the 25 basis points it had previously telegraphed.

Profit-taking also may have contributed to the recent pullback, as Morgan Stanley’s FX market positioning tracker showed that the long-dollar trade had become exceptionally crowded in recent weeks, which can often be an indicator that a recent swing is about to reverse.

Extreme strength

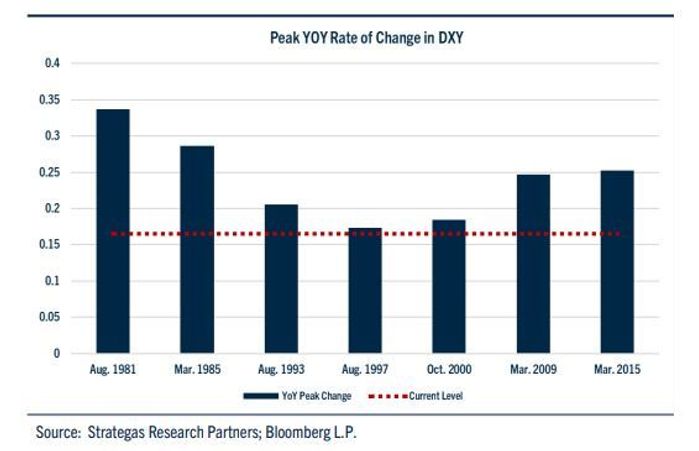

Looking for answers in history, John Lynch, the chief investment officer at Comerica, examined how stocks, bonds and commodities performed during previous bouts of extreme dollar strength. Investors might be intrigued by his findings.

Source: Comerica

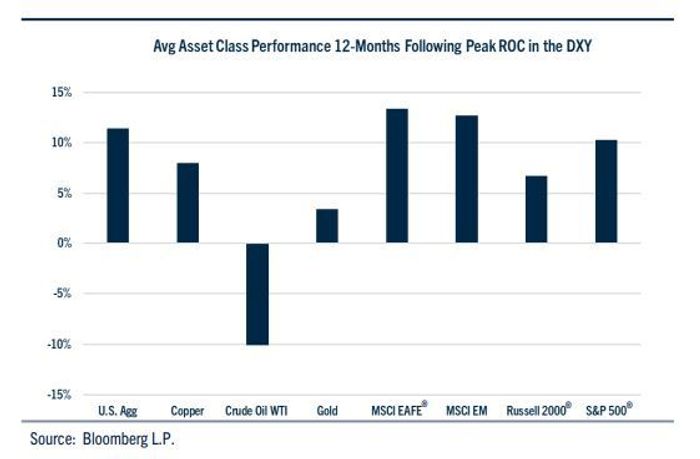

While dollar strength has often corresponded with periods of weakness in equities, Lynch points out that there is a light at the end of the tunnel. During the 12 months following a cycle peak for the dollar, equities of nearly every stripe (with the exception of energy stocks) have outperformed.

For starters, there is reason to believe that the greenback’s long-winded rally isn’t over yet. The ICE U.S. Dollar Index has, on average, risen by 24% during periods of appreciation, including the yearlong stretches that ended in August 2000 and March 2015.

Global markets undergo relief rally as dollar exhausts gains

According to Lynch, “over the past 40 years, once the U.S. dollar had peaked, the S&P 500 climbed by an average of 10% over the ensuing twelve months as investors embraced a risk-on environment.”

Lynch found that consumer discretionary stocks and financials outperformed during the year after the dollar’s peak.

Source: Comerica

But the gains weren’t limited to U.S. markets. Lynch found that emerging markets and developed markets both rallied in the wake of the dollar’s strength. Crude oil was the only exception, which would seem to clash with the conventional wisdom that a weaker dollar should help lift prices of industrial commodities like oil, Lynch wrote.

Source: Comerica

Even Lynch acknowledged that while Comerica sees the dollar as likely close to its peak, there could be more upside ahead.

“The Fed has a long way to go in its battle against inflation,” Lynch told MarketWatch. Although global investors have “almost reflexively” parked their money in the dollar to shelter it from crashing equity and bond markets, Lynch also wonders whether a recession in the U.S. might help to diminish some of the dollar’s appeal.

‘Dollar doom loop’

While the U.S. economy is largely insulated against the strong dollar, prolonged strength could create strains in the international financial system. As Standard Bank’s Steven Barrow explained to clients in a research note earlier this year, the strong dollar forces other economies to “import” inflation by increasing the costs of foreign goods, while also raising the cost of currency hedges.

It also makes it more difficult for sovereign governments that borrowed in dollars to pay down their debts, making them more vulnerable to financial crises like the “Asian flu” of the late 1990s.

Jon Turek, founder of JST Advisors, a research shop that works with hedge funds to develop macro trade ideas, wrote on his substack “Cheap Convexity” about the threat of the “dollar doom loop”. This happens when the strong dollar depresses global trade, which in turn depresses growth in other developed markets (like Europe) relative to the U.S.

According to Turek, this cycle risks becoming self-reinforcing, with dollar strength continuing to beget dollar strength until it triggers a global meltdown.

The euro EURUSD traded at 1.02 to the dollar on Wednesday, and the Japanese yen USDJPY traded at 138 yen to the dollar, which is just shy of the greenback’s strongest level against the Japanese currency since 1998.

Stocks rose Tuesday, with the Dow Jones Industrial Average

DJIA,

gaining around 48 points, or 0.2%, as major indexes built on a broad Tuesday rally. The S&P 500

SPX,

finished with a gain of 0.6%, while the Nasdaq Composite

COMP,

jumped 1.6%.

{kind=link}